What is a virtual bank?

A virtual bank is a bank that primarily delivers retail banking services through the internet or other forms of electronic channels instead of physical branches. Consumers can open a virtual bank account and use other banking services via mobile apps, mostly facilitated by financial technology (also known as “fintech”). However, virtual banks are also required to set up a physical office in Hong Kong as the principal place of business to, inter alia, engage with customers, handle enquiries and complaints, and should not impose any minimum balance requirements or charge low-balance fees.

Virtual banks generally target the retail segment, including small and medium-sized enterprises (SMEs). Virtual banks are subject to the same set of supervisory requirements applicable to traditional banks, though certain requirements may be adjusted, under a risk-based and technology-neutral approach, to suit the business models of virtual banks.

Is virtual banking suitable for you?

Let’s find out by answering 3 simple questions:

1. Do you require investment services or mortgages?

2. Do you frequently make deposits in cash / cheques / cashier’s order?

3. Do you opt for making visits to branches for in-person services?

If your answer is ‘yes’ to any of the above, then virtual banking may not be able to address all your needs. Let’s find out why:

Types of service | In the early establishment of virtual banks, services available are limited to savings deposits, time deposits, and local money transfers. Some also include other services such as debit cards, credit cards, foreign currency exchange and loans. Nonetheless, virtual banks do not render general services that traditional banks do, such as cheques, mortgages, and investments, etc. |

Deposits and withdrawals | Traditional banks usually take deposits in cash, cheques, cashier’s orders or via bank transfers. Contrarily, with no physical branches, virtual banks are unable to take deposits in cash, cheques or cashier’s orders. Account holders can only make deposits through bank transfers. Furthermore, unless the virtual bank provides debit cards to facilitate payments at designated merchants or allow cash withdrawals at designated ATMs, account holders will have to first make a transfer from the virtual bank to another bank before the funds can be used, which can be time consuming. |

No physical branches | As virtual banks do not have any physical branches, in case a customer wants to communicate with a bank personnel, under normal circumstances, that could only be done through instant messaging via the mobile apps or calling the hotlines. Customers are unable to make face-to-face enquiries at bank branches. What's more, if account holders have unfortunately lost their mobile phones or if their phones fail to function properly, they will not be able to use the banking services until they have a new phone or have the faulty one repaired. |

*Debit card: It is an ATM card linked to a bank account, which can be used to withdraw money from the bank account through ATMs of designated networks (e.g., JETCO) and make payments at merchants. Cardholders can also withdraw money at designated merchants through EPS or pay for goods bought online. In addition, debit card can be used to make transfers, pay bills and check account balances.

Before using a debit card, consumers must deposit money into the bank account. Subsequent withdrawals or spendings using the card will be debited directly from the account. Transactions will normally be declined when the bank account does not have sufficient fund, thereby preventing the cardholder from spending beyond means.

| Traditional Banks | Virtual Banks | |

|---|---|---|

| Customer segment | All | Mainly retail customers (including individuals and SMEs) |

| Channels | Branches / ATMs / automated banking machines / telephones / Internet / mobile apps | Mainly via mobile apps; some virtual banks provide withdrawal services via designated ATMs, or certain banking services via telephones or the Internet. |

| Business hours | Depending on the channels and types of services, some services are only available during banking hours; however, most services are available 24/7 via online banking, mobile apps, or through some of the automated banking machines. | Most of the services are available 24/7 (However, currently some services, e.g., foreign exchange and loans are only available during specified hours). |

| Services | Comprehensive banking services including deposits, withdrawals, time deposits, local transfers, telegraphic transfers, cheques, foreign exchange, mortgages, loans, insurance, credit cards, and investments. | Currently, services mainly consist of deposits, withdrawals, time deposits, local transfers, and debit cards. Some virtual banks also provide individual and SME loans, credit cards, foreign exchange, and insurance. |

| Account opening procedures | Customers can open bank accounts and undergo identity verification at the branches; some banks offer remote account opening via mobile apps. | Mainly done remotely via mobile apps. |

| Required documents for account opening | For opening savings or deposit account, normally an ID should suffice; for applying investment account or loans, residential address proof and other documents may also be required. | |

| Cash withdrawals |

|

|

| Account balances and charges | A majority of retail banks have eliminated below balance fees on most types of accounts; certain account types may still have minimum balance requirements and associated below balance fees | No minimum balance requirements or below balance fees |

| Supervision | By the Hong Kong Monetary Authority (HKMA) | |

| Network security / data protection | Pursuant to the Supervisory Policy Manual of HKMA, banks are required to implement adequate IT control measure to safeguard the confidentiality and completeness of data, especially the confidentiality of customers’ data. Banks are required to adhere to the ‘fit for purpose’ principle, i.e., the security measures and technologies adopted by banks are required to be commensurate with the risks associated with the underlying transactions. | |

| Deposit protection | Under the Deposit Protection Scheme, deposits placed with each member bank are protected up to HK$500,000 per depositor | |

| Note: The above is only a general summary of the typical differences between traditional banks and virtual banks. Individual banks may vary in their product/ service offerings. | ||

Details about virtual bank accounts

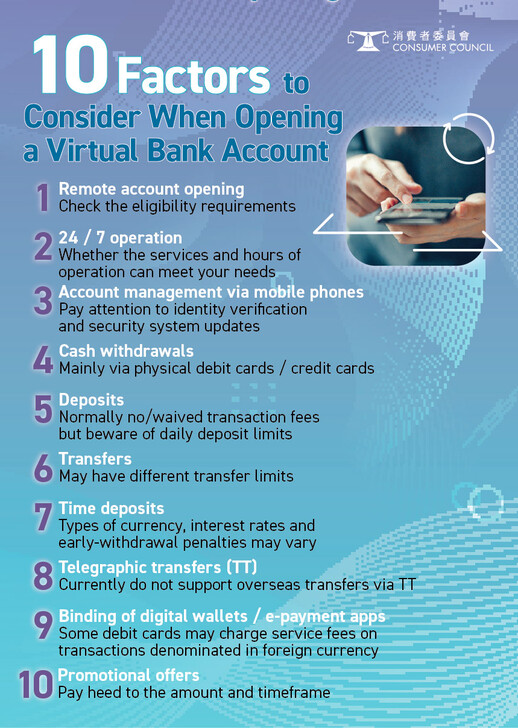

If you think virtual banking is suitable for you after careful consideration, the next step is bank selection. The Consumer Council (or the ‘Council’) previously conducted a survey on 8 virtual banks in Hong Kong and consolidated the following factors which you may consider when comparing services amongst different virtual banks:

Eligibility criteria for account opening

To be eligible for opening a virtual bank account, one must be aged 18 or above and must be a holder of Hong Kong ID. Most of the banks indicated that they could not open bank accounts for U.S. citizens, individuals who were tax residents of the U.S. or other jurisdictions outside Hong Kong. Besides that, the 8 banks shared similar account opening procedures, which involved downloading the bank’s mobile app, verifying one’s mobile phone number, uploading ID card, activating facial recognition function (by taking selfies), and providing personal details. It was also noted that all the virtual banks in Hong Kong do not charge a fee on account opening.

Interest rates on deposits

All the virtual banks surveyed took savings deposits in Hong Kong Dollars (HKD) while only a few of them took deposits in Renminbi (RMB) and US Dollars (USD) as well. Consumers should be aware that the high interest rates offered by banks on deposits might have conditions attached, e.g., such rates might only be applicable to new customers who opened bank accounts during a specified period and deposited a particular amount within a specified timeframe, and such rates might drop substantially afterwards. Most of the virtual banks offered different interest rates depending on the deposit amount. The frequency of interest distribution also varied among banks, some paid daily interests whereas some paid monthly interests.

Only 4 out of the 8 virtual banks offered time deposits services. Among the 4 banks, 1 provided only HKD time deposits, while the other 3 also provided RMB and USD time deposits. Some banks determined the annual interest rates on time deposits based on the number of partakers, the more the partakers, the higher the interest rates. Consumers should also be aware of charges and consequences on early redemption of time deposits. In some events, the interests might be forfeited.

Maximum transfer limits

All the virtual banks surveyed accepted real-time deposits and transfers through the Faster Payment System (FPS), and accepted deposits via the Real Time Gross Settlement System (RTGS) (also known as the Clearing House Automated Transfer Systems (CHATS)). Some banks also provided specific options for deposits / transfers. It should be noted that if deposits were to be made from other local banks under direct debits (i.e., via Electronic Direct Debit Authorisation (eDDA)) to the virtual bank accounts, despite being free of charge, there would generally be a daily deposit limit, ranging from HK$30,000 to HK$500,000.

All the surveyed virtual banks imposed a daily outward transfer limit, ranging between HK$200,000 and HK$1 million. The limits depended on certain factors, such as completion of the bank’s internal assessment process, mode of transfer, and whether the recipient was a registered account with the virtual bank or an account under the same name as the transferer, etc.

Among the 8 virtual banks surveyed, only 1 of them accepted deposits from overseas transfers, and such service was free of charge and did not have any transfer limits in place.

Cash withdrawals

As outlined above, some virtual banks provided withdrawal services via debit cards / credit cards with daily withdrawal limits ranging from HK$20,000 to HK$50,000. However, these services might not be free of charge, e.g., some banks charged HK$20 – HK$30 for every withdrawal made via the Mastercard ATM network, some banks charged HK$20 plus a foreign transaction fee for every foreign currency withdrawal via the Visa ATM network. Some of the banks provided cardless withdrawal services via designated ATMs for free.

Binding of digital wallets / e-payment apps

Most of the accounts and debit cards provided by the virtual banks allowed the binding of certain digital wallets / e-payment apps, such as Alipay HK, Apple Pay, and Google Pay, etc. Consumers can go through the list to determine which bank can better support their payment habits.

Spending rebates

To encourage spendings by account holders, virtual banks that issued debit cards or credit cards normally did not charge any annual fees, and would offer certain spending rebates to consumers. However, the criteria for receiving these promotional offers and the maximum limits differed across banks, e.g., some banks would offer cash rebates of 1% - 8% depending on the categories of spending, others might determine the rebate amount through lucky draws. The maximum limits varied from HK$250 per month to HK$10,000 per transaction. Consumers should beware that the promotional offers are subject to change, as such they should not spend beyond their means for the sake of such offers.

Furthermore, no matter using traditional banking or virtual banking services, consumers should always keep their mobile phones safe, update the operation and security systems of the phones, as well as the mobile apps of the relevant banks from time to time. Consumers should also beware of computer viruses and hackings.

Last but not least, closing a virtual bank account is more than just removing the mobile app. The account holder should first transfer the funds to another bank account, download the e-statement or notifications for record, then notify the virtual bank’s customer service team to arrange for the closing of the account.

For more information, please refer to the article ‘A Comprehensive Review on Virtual Banks Conditions Attached to the High Interest Rates and Rebates’ (Chinese version only) in Issue #537 of the CHOICE Magazine.

![[Baby Snacks Guide] Who Says Snacks Can’t Be Healthy?](/f/guide_detail/415742/376c212/bb%20snack.jpg)