Introduction

- The Consumer Council (CC) is pleased to provide views from the consumer’s perspective to the LegCo Panel on Financial Affairs concerning the impact of branch closure of banks on the public. This paper also summarizes the Council’s survey findings concerning branch closure of banks in Hong Kong which was released in the June 2006 issue of its Choice magazine.

Survey Findings

- In May this year, CC conducted a survey on 23 banks in Hong Kong in relation to changes in banks’ fees and charges, as well as the closure of bank branches. The findings were compared to those obtained in a similar survey conducted in 2001.

17% Reduction in Bank Branches

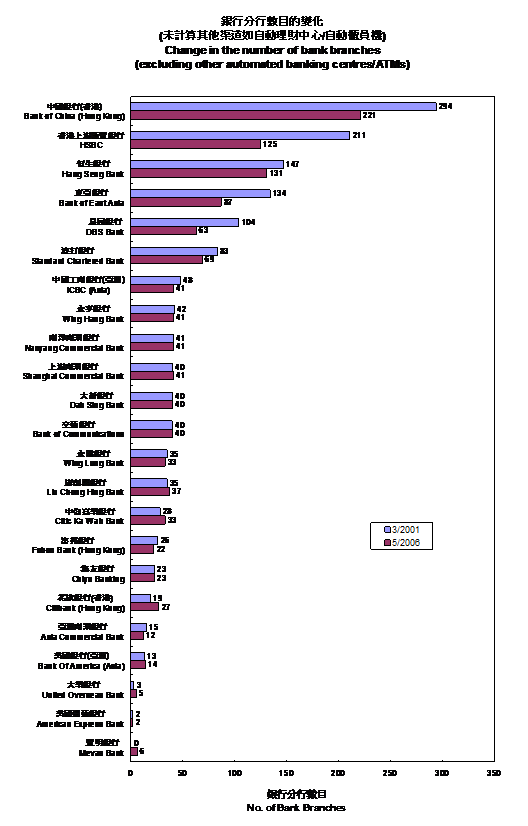

- In addition to fee rises, the survey found fewer retail bank branches these days. The survey showed a progressive phase out of bank branches over the years from 1,463 in 2001 to 1,209 in May this year, an overall reduction of 254 branches or 17%.

- Some branch closures were due to consolidation and merger between banks, while others substituted by new banking centres in other areas. Such a phenomenon is set against the background of intense growing competition in the banking industry following the deregulation of interest rates in 2001, and banks may have closed branches to achieve optimum economic efficiency. On the other hand, it should be recognized that market liberalization has brought benefits to the consumers due to a narrowing of the interest rate spread as interest rates for depositors went up and rates for debtors came down. This said, the impact of branch closure of banks on the public needs to be examined.

- Compared to 2001, 11 of the 23 banks surveyed have reduced their branches by 2% to 41%. But not all banks have followed this trend. Six in fact have expanded the number of branches from 3% to 67%. Table 1 in the Appendix shows the number of branches by individual banks in the years 2001 and 2006.

- Against this background of fewer bank branches has emerged an impressive growth in the number of ATMs, and online banking transactions. Figures from the Hong Kong Monetary Authority (HKMA) and the Hong Kong Association of Banks (HKAB) suggest that consumers are increasingly turning to such new banking services. According to the HKMA, the number of personal online banking accounts has grown from 1.1 million in 2001 to 3.3 million in 2005. A remarkable threefold increase.

- Despite the benefits, some segments in our community are unable to take advantage of the newer forms of banking services made possible through technological advancement.

Taking a district perspective

- Table 2 of the Appendix to this paper sets out the availability of bank branches with counter service by district, population and household income. There does not seem to be an overall relationship between branch number and population or income suffice to say that branch distribution is spatially uneven. Granted that there are a number of factors underlying a bank's decision for its geographical network, e.g. the bank’s business strategy, customer profile, business opportunity presented etc. it takes a more detailed field study at the district level to gauge the accessibility of banking services to the average consumer and to specific pockets of population. CC considers it a worthwhile exercise for local NGOs and concerned parties to undertake such a study.

- Whilst most consumers may still access banking services near their workplace or via other electronic means, this might not be the case for the elderly, people with disabilities and economic disadvantaged groups.

- Reduction in bank branches will affect these groups who, for one reason or another, will not be able to use online banking or effect transactions through ATMs. ATM machines present great problem to some senior citizens because of their slow motion and inability to remember pin numbers. People with motion disabilities will also suffer from closure of a nearby branch. For the economically disadvantaged, computers are not easily accessible to them for online banking.

Access to banking services

- Indeed, it is the commercial decision of individual banks to decide on the number and location of their branches. Yet in an advanced economy and an international financial centre such as Hong Kong, banking service has become a basic need in the daily lives of people. The issue of physical access for those who are not using electronic transactions therefore needs to be addressed by the banking industry and by our community as a whole.

- CC understands that the HKAB has set up a working group to explore measures to cater for this community need. According to the HKAB’s press release dated 23 June 2006, the industry is looking into ‘the feasibility of enabling cash withdrawals on a limited scope basis, independent of any purchase of goods, at selected chain retailers with EPS payment facilities.’ CC hopes that such co-operation between commercial concerns will work out to the convenience of banking consumers particularly those with special needs as mentioned above.

- CC also suggests that individual banks may also look into the feasibility of using other methods of personal identification e.g., retinal or finger prints to facilitate use of ATM banking by senior citizens with minimized risk, unless the costs is so phenomenal as to become unrealistic.

- Accessibility is not just about location of bank branches or availability of services via different means, affordability also poses barrier to access to banking service. The same CC survey also found that in comparison with 2001:

- more banks require account opening deposit, from $1,000 to $3,000 (5 banks), $500 (1), $100 (5) and $0 to $10 (12);

- 18 of 23 banks have begun to reduce interest rate payment on low balance, with 12 of them even adopting zero interest rate policy on such accounts;

- more banks now charge separately for inactive accounts and low-balance accounts – from only 2 banks in 2001, the number has risen to 18, and the low balance account charges range from $10 to $200 per month.

- In the latter case, 16 banks offer to waive such a charge to the elderly and disadvantaged groups. Whilst the upward trend is obvious, with the relief measures offered by some banks, the issue of financial exclusion does not appear to be a big problem generally as yet. Still this is an issue to be closely monitored.

Experiences in Other Economies

- In advanced economies such as Canada, UK and the US, there are provisions to ensure consumers’ access to basic banking service, for example, banks must provide a basic account which attracts no keeping fee and provides limited free transaction services per month. In Canada and the US, closure of bank branches must follow a set procedure. In the case of the US, in its evaluation of a bank’s performance and the assignment of ratings, the regulator will consider, among other factors, a bank’s record of opening and closing branches, the effect of those openings and closings on the communities in which the branches are or were located, and public comments received on branch closings.

Conclusion

- Such overseas experiences may serve as useful reference for Hong Kong in case a need should arise in future. CC awaits the proposal from HKAB to minimize the impact of branch closures to consumers.

- Meanwhile, CC believes authorities concerned would welcome feedbacks from NGOs and concerned parties on the special needs and particular circumstances in their respective communities/districts.

- CC believes that the Deposit Insurance Scheme, once in operation, should enhance consumer confidence in licensed banks and hence enlarge the number of banks that consumers are prepared to choose from. Consumers may feel more at ease to choose the service from banks which best suits their needs and are convenient to them.

- Finally, CC trusts that HKMA and HKAB as regulator and industry association will keep the matter in view in order to ensure basic banking service is available to all.

Appendix

Table 1: Number of bank branches

Source: Data supplied by individual banks.

Table 2: Number of bank branches, population and household income by district

| District | No. of local branches* (As of 23 May 2006) | 2005 Population | Median monthly household income (HK$) | |

|---|---|---|---|---|

| Overall | Age≥65(% share) | |||

| Central & Western | 136 | 247,600 | 28,400(11.5%) | 24,900 |

| Wanchai | 109 | 150,500 | 23,700(15.7%) | 25,000 |

| Eastern | 125 | 585,900 | 78,800(13.5%) | 20,000 |

| Southern | 30 | 270,700 | 36,800(13.6%) | 19,000 |

| Mong Kok | 57 | 302,000 | 42,400(14.0%) | 15,000 |

| Yau Tsim | 105 | |||

| Sham Shui Po | 78 | 372,100 | 60,100(16.1%) | 12,200 |

| Kowloon City | 81 | 370,900 | 51,300(13.8%) | 18,500 |

| Wong Tai Sin | 50 | 431,300 | 67,100(15.5%) | 13,700 |

| Kwun Tong | 84 | 585,700 | 90,800(15.5%) | 13,000 |

| Kwai Tsing | 46 | 511,700 | 60,500(11.8%) | 14,000 |

| Tsuen Wan | 52 | 277,400 | 37,800(13.6%) | 19,000 |

| Tuen Mun | 39 | 495,400 | 34,900(7.0%) | 14,200 |

| Yuen Long | 40 | 550,200 | 40,500(7.4%) | 13,000 |

| North | 32 | 289,800 | 30,000(10.4%) | 15,000 |

| Tai Po | 31 | 298,000 | 29,200(9.8%) | 15,500 |

| Sha Tin | 67 | 617,000 | 62,400(10.1%) | 18,000 |

| Sai Kung | 28 | 403,900 | 28,900(7.2%) | 20,000 |

| Islands | 19 | 130,200 | 12,000(9.2%) | 15,000 |

| Overall | 1,209 | 6,890,300 | 815,700(11.8%) | 15,800 |

Note:

* Local branch is defined in section 2 of the Banking Ordinance (BO). In essence, it means a place of business in Hong Kong, at which a bank carries on banking business; or any other business whereby it may incur financial exposure mentioned in section 81(2) of the BO. Banking business is defined in section 2 of the BO as “the business of either or both of the following - (a) receiving from the general public money on current, deposit, savings or other similar account repayable on demand or…; (b) paying or collecting cheques drawn by or paid in by customers”. The definition of local branch does not include the “principal place of business in Hong Kong” of a licensed bank.

Source:

Branch figures are provided by the Hong Kong Monetary Authority.

Population statistics are obtained from the Census & Statistics Department.