Financial products for retirement protection have been flourishing in view of the aging population. Annuity products and in particular the recent tax deductible Qualifying Deferred Annuity Policies (QDAP), certified by the Insurance Authority, have further encouraged consumer demand for retirement annuity cover. In a survey on 37 different annuity plans, the Consumer Council has found vast variations among the plans in areas such as issuing age, premium, payment periods and rate of return of QDAP, etc. For instance, the guaranteed internal rate of return could range from 0.01% to 3.05%; the guarantee payback period could range from 5 to 26 years; and the annuitisation period could span from 4 years to lifelong. Before making a decision to purchase, consumers should first review their age, financial condition, affordability, family members and quality of retirement life to assess their payment ability and the contribution period. Furthermore, they should carefully compare the different annuity options to choose the product that suits them most.

Annuities are long-term life insurance products to prepare the insured for their retirement life. There are lot of products available and their terms are complicated with some annuities having premium payment period spanning for more than 10 years. Consumers buying aggressively beyond their ability will not only fail to give the retirement protection they need, but early surrender or termination of the plan may also result in severe financial loss. For those insured but surrender the policy upon expiry after the first year, the surrender value of some QDAP plans could be down to a mere 14% of premiums paid; likewise, the surrender value of 6 general annuities could be reduced to 0%, implying the forfeiture of all premiums they have made to the annuity fund.

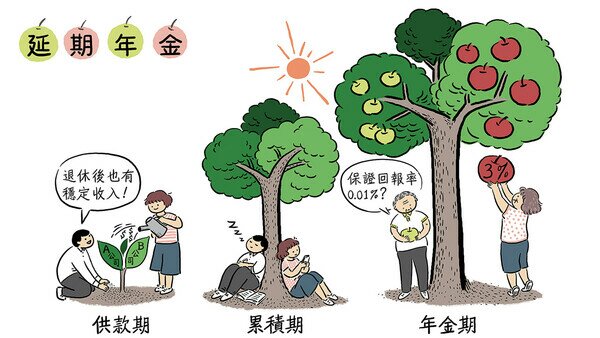

Generally speaking, annuity policyholders are obligated to pay all required premiums within the “premium payment period”, and over the “accumulation phase”. Insurance companies will, through investment, keep growing dividends on their policy value till the “annuity period” when the insured will be able to draw annuity income progressively according to their needs. Assume purchasing annuities with equivalent amount of investment, the sooner the premium payment commences, the shorter the annuity period and the later the payment of annuity begins, a higher amount of income the insured will receive.

The Council collected and analysed a total of 37 annuity plans from 18 insurers, of which 12 were QDAP and 25 were general annuities. QDAP plans must meet established criteria, including minimum total premium contribution of $180,000; contribution period of a minimum 5 years; annuity period of at least 10 years; insurers must disclose the internal rate of return and clearly present the amount of both the guaranteed and non-guaranteed annuity income; and the insured must reach the age of 50 to be eligible for the receipt of annuity payments.

General annuities are based on the premium payment mode and accumulation period and further divided into “immediate annuity”, “deferred annuity”, “annuity certain”, and “life annuity”. Take the example of the Hong Kong Annuity Co. Ltd. offering Hong Kong permanent residents of age 65 or above the “Hong Kong Annuity Plan”, the product is a “life annuity” and once all the premiums are settled one-off with a lump sum, the money will be converted to a stable source of cash flow, and the insured would not have to wait for the “accumulation period” before drawing annuity every month till death.

Policy issuing age

The survey found significant difference in the lowest/highest issuing age of applicants. Among the 12 ODAP plans, 5 plans set the lowest issuing age at 18 years, and the upper limit of issuing age ranges from 50 to 75. Among the 25 general annuities, the lowest issuing age ranges from age 0 (3 plans) to 15 days after birth (11 plans) while the upper limit between 55 and 80 years.

Should, unfortunately, the insured die during the policy period, all QDAP will offer death benefit. If the total premiums fall below the limit set by the insurance company, 8 plans do not require the insured to undertake medical checkup or produce health information; 4 plans do not set any premium limit and waive the need for the insured to undertake medical examination.

Premium payment period

In the survey, QDAP generally offer premium payment period of 5 or 10 years and the longest up to 15 years, for plans that offer 5-year premium payment period, annual minimum premium ranges from $36,000 to $98,000. For general annuities, the difference among the plans in premium contribution period was found considerable since there are no stated restrictions imposed with some plans allowing payment with a lump sum, or the premium contribution period to be spread from 2 to 62 years while others are calculated on age with contribution period till the age of 60 or 65.

Annuity period

Among the 12 QDAP plans, the annuity period is generally 10 to 20 years, but 1 plan offers up to even whole life of the insured. The annuity period of general annuities offers more flexible choices. Among the 25 plans, 2 are for life, and 11 plans offer annuity up to age 100 or above with the longest one set at age 130.

Information transparency and rate of return

In regard to product information transparency, QDAP plans are required to disclose the IRR, including the guaranteed IRR and total IRR as well as separately disclosing the guaranteed and non-guaranteed annuity incomes to facilitate the insured in comparing the rate of return of different products. However, most general annuities plans will display the total return as a percentage of the total premiums paid to indicate the rate of return but such practice cannot reflect the time value of the premiums paid that represents the time lapse between completion of all premium payments and the commencement of annuity distribution for which consumers should beware in the choice of annuity.

The rate of return is a crucial factor in the consideration of an annuity. The survey found significant variations in the guaranteed internal rate of return (IRR) among the QDAP plans ranging from 0.01% to 3.05%, due mainly to variations in the length of the accumulation period of different plans. Consumers should therefore compare plans with closely similar accumulation periods. Based on the average inflation rate of about 2% to 4% in the past 10 years in Hong Kong, the guaranteed IRR of the majority of annuity plans is generally lower than the inflation rate.

Among the 12 QDAP plans, 6 offer the choice of policies in the currency of HKD, USD or RMB. For policies of 5-year premium payment period and 20-year annuity period, the guaranteed IRR offered by HKD policies ranges from 0.62% to 1.30% while those offered by USD policies ranges from 0.62% to 2.72%. Though the IRR offered by USD policies is relatively higher than those offered by HKD policies, consumers should be wary about the risk of the currency exchange rate that may affect the substantial return.

Many consumers are also concerned about the “non-guaranteed” actual performance. They may refer to the dividend ratio provided by the insurers, comparing the actual fulfilment distributed on the policy to the dividend sum outlined in the sales document. The amount of dividend distribution is influenced by multiple factors, such as investment return, financial status, claims rate, policy renewal rate and operating overheads, etc.

In choosing annuity plans, consumers should take heed of the following:

- Annuities are insurance products based on dividend distribution, the amount of dividend distribution is affected by many factors and solely decided by the insurers. Consumers should choose annuity products that offer higher “guaranteed” rate of return. Early surrender may result to the policyholders in a surrender value that is far below the premiums paid and heavy financial loss;

- For those without a steady job or income, they may consider taking out annuity that offers premium holiday or deferred payment. Should they face financial difficulty, they can apply to the insurance company for temporary deferred premium payment to avoid termination of the policy due to payment default;

- Premiums can be paid annually which is cheaper than paying monthly or other payment mode. The insured should evaluate their own consumption and saving patterns to choose the payment mode suitable to them. For those who live from paycheck to paycheck with weaker self-discipline are probably better off with the monthly mode;

- Some annuity plans do not require the insured to produce proof of their health conditions. Retirees or the elderly therefore need not worry about their health conditions or undertake medical checkup in order to convert their capital into a stable stream of cash flow during retirement;

- The IRR contained in annuity product brochure is subject to change in accordance with a host of factors, including the insured gender, issuing age, policy currency, premium payment period, accumulation period, annuity period, premium payment mode, or commencement age for annuity income, etc. Consumers should take it for reference only.

The Consumer Council reserves all its right (including copyright) in respect of CHOICE magazine and Online CHOICE.