The residential property market boom with prices rising to ever new record high has not dampened the buyers’ interest. Long queues of buyers appear whenever a new property is launched on the market. However, there have been prospective buyers of first-hand residential properties who had their deposits forfeited due to various reasons including unsuccessful mortgage loan approval. Prospective buyers are reminded to compare prudentially the various mortgage plans in the market to have a clear grasp of the interest and different fees and privileges. What appears to be quite similar may differ vastly in interest charges of $100,000 or above.

Before purchasing a property, prospective buyers should avail themselves to the online mortgage calculator and the free mortgage preliminary assessment services provided by some banks to evaluate their repayment ability and likelihood of their mortgage application being approved. Never sign in haste a provisional sales and purchase agreement and pay a deposit as in the event of your mortgage being turned down or only partially approved and your inability to pay the extra down payment, you may end up with “deposit forfeiture”. The Consumer Council highlighted that there are many factors that could affect the outcome of your mortgage application. Although banks have to abide by the rules of the authorities in mortgage approval, individually they also set their own requirements and standards. Prospective buyers should shop around for comparison; you may be rejected by one bank in your application but another bank may well find you acceptable for mortgage approval.

In a survey last month, the Consumer Council approached 21 banks in Hong Kong for information about residential property and carpark mortgages. 17 banks responded with a total of 69 mortgage plans of various types: HIBOR mortgage plan, Prime-based mortgage plan, Mortgage Insurance Programme, Government Home Ownership Scheme, Tenants Purchase Scheme and carpark mortgage plan.

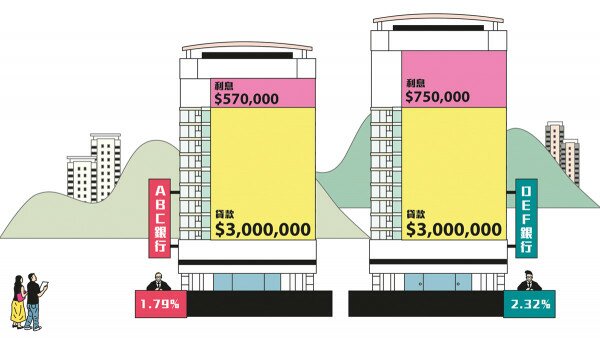

In choosing a mortgage plan the interest rate is naturally a major factor for the buyer as it affects directly the instalment amounts in the years ahead. On the basis of the interest rates on August 22, the interest charge of the HIBOR plan ranged from 1.79% to 2.32%, while that of the Prime-based plan 2.15% to 2.25%. Assuming the Prime and HIBOR remain unchanged during the repayment period, if a purchaser buys a flat of $5 million with a mortgage loan of 60% or $3 million to be repaid over 20 years, the monthly instalment with interest calculated at the lowest rate of 1.79% will amount to some $14,900; the full interest costs amount to about $570,000 in total. Whereas if calculated at the highest interest rate of 2.32%, the monthly instalment would be about $15,600 and the full interest costs some $750,000, a significant difference in interest charges of nearly $200,000.

In addition, property developers are also offering mortgage plans with high loan-to-value ratios to attract buyers who are otherwise possibly unsuccessful in applying for bank loans. But these mortgage plans come with a high interest rate doubling or even more than those charged by banks; the total interest costs could amount to a few million dollars more. Prospective buyers should take a comprehensive assessment of their own repayment ability before making any decision.

For example, in the case of a flat priced at $8.48 million, under the mortgage plans of the traditional banks, they are required to follow the guideline of Hong Kong Monetary Authority (HKMA which sets the loan limit at $5 million, so the buyer has first to pay a down payment of $3.48 million. Calculated at an interest rate of Prime-2.75% and repayment period of 25 years, the total interest costs would come to about $1.54 million, the monthly instalment would be about $21,000 per month. But under a developer’s mortgage plan which offer loans up to 80% of the property value (i.e. $6.78 million) with the interest calculated at a Prime+1% interest rate and repayment of interest only in the first 3 years over the same repayment period of 25 years, the total interest costs would come to a high $6.67 million, which is $5 million more than the mortgage plans of traditional banks! In the first 3 years, the monthly instalment would be about $33,000 and the remaining 22 years the monthly instalment would rise to $46,000, doubling that of a bank mortgage loan.

Consumers who don’t have enough savings for down payment and opt to choose this type of mortgage must be very careful about their repayment ability in the years to come, and the final total interest expenditures. Besides taking into consideration if the time is right to make property purchase and its price, always compare other mortgage options that are open for your choice.

Prospective buyers who do not have enough savings to pay for the 40% down payment, could take out the mortgage insurance covers offered by the Hong Kong Mortgage Corporation or other insurers – thereby raising the mortgage loan to a higher ceiling of 90% of the property value. But buyers should take heed of the restrictions: the value of the property to purchase must not exceed $4 million; the applicants must be a first-time buyer with stable salary and hold the property in his or her own name for personal use, and the repayment ratio must be lower than 45% of income.

Besides interest rates, consumers should also factor in for consideration the banks’ various privileges and service charges as well as the restrictions in individual plans. All but one of the 17 banks offered cash rebate up to 1% to 1.6% of the loan amount. But prospective buyers should be aware that the HKMA stipulates that if the cash rebate exceeds 1% of the loan, the sum of the rebate must be deducted from the loan amount thus effectively reducing the mortgage loan a prospective buyer could obtain. Further, banks generally would release the cash rebate only afterwards when all the mortgage procedures have been completed, and in the event of early redemption within a stipulated period, a partial or full refund of the cash rebate may be required.

Further, 3 of the banks would levy a mortgage application service fee – 2 charging 0.25% and 0.5% of the loan amount and the other one a set amount of $1,000 to $2,000. Almost all the banks would charge a service fee for early redemption – 4 of them charging between $500 and $1,000 per early redemption while the rest charge, within the first 4 years, 0.5% to 3% of the total loan or the amount of early payment; some banks have set a minimum charge. In the case of a mortgage loan of $3 million, for example, some banks would charge a set sum of $500 for early redemption of the whole loan, but others would levy, if the early redemption was within the first 3 years, a high 3% service charge of the entire mortgage loan i.e. $90,000.

When choosing a mortgage plan, prospective buyers are advised to pay heed to the following:

- Prospective buyers should be prepared with some fund in reserve for the rainy days to tide over difficult times such as work, family or health problems;

- Consider various repayment options that best suit your ability and cash flow, for instance, choose repayment on a monthly basis or alternatively every other 2 weeks may reduce interest charges.

The Consumer Council reserves all its right (including copyright) in respect of CHOICE magazine and Online CHOICE.