- Auto-fuel prices have a major impact on the Hong Kong economy. Household and commercial drivers are directly impacted by the pricing of the auto-fuel products in the market. Furthermore, as transportation cost is passed through into the prices of all goods, it also indirectly affects most of economic activities in Hong Kong.

- In Hong Kong, consumers noted the drastic decline in the international crude oil prices but did not see an equivalent reduction in auto-fuel prices. There were challenges that the oil companies were profiteering by not passing on the reduction of international crude oil prices fairly to consumers.

- In this report, the Consumer Council (the Council) examines practices in the pricing of auto-fuel. The Council is presenting its findings with regards to oil companies’ pricing practices in the auto-fuel products market. The Council believes the analysis provides the public with a better understanding of auto-fuel price movement and helps the Government decide on any further measures to safeguard the interest of consumers.

Objectives and Methodology

- Analysis was undertaken examining the relationship between the pump price (before discount) of the five oil companies and the international (Brent) crude oil price from daily prices between January 2013 and December 2014.

- The Council was looking for signs of the following pricing practices:

- “Quick going up, slow coming down” - whether the pump price changes more quickly when international crude oil price rises, and more slowly when it falls.

- “More going up, less coming down” - whether the pump price increases more in respond to an increase in international crude oil price and decrease less in respond to a decrease, i.e. the gap between pump price and international crude oil price rises over time.

- “Quick going up, slow coming down” - whether the pump price changes more quickly when international crude oil price rises, and more slowly when it falls.

- The study only analyses the data collected publicly. The Council does not have access to price data for every shipment of auto-fuel imported into Hong Kong but only import price data that consolidates all imports in that month. There are limitations of using the international crude oil as a proxy for the underlying input cost of the auto-fuel product. But given that the imported oil price is highly correlated with international crude oil price (correlation coefficient = 0.89), the Council is confident that its observations are still valid.

- There are a couple of points worth making about the approach of using the differences between the pump price and the international crude oil price as a proxy for companies’ product cost margin. Firstly, oil is imported into Hong Kong as petrol and diesel, not crude oil. If the cost of refining is reasonably fixed over the period this is not a serious problem for our analysis. Secondly we have no access to cost data of oil companies. As a result a precise understanding of how the product cost margin for gasoline related to the profitability of the company could not be estimated. In addition, market share and marketing programmes of each oil company is also not available to gauge the effect of pricing practices to the public.

The Findings

- The average pump price is the aggregate average of the 5 oil companies in Hong Kong. It is noted that both the Brent crude oil price and the average pump price drop significantly in the 2nd half year of 2014. It is observed that the magnitude of percentage change is larger (53.9 points drop) in the Brent crude oil price than the average pump price (24.1 points drop) between 1 Jul 2014 and 31 Dec 2014.

- The Council found that the price gap increased by around 48 cents per litre (increased by 8.7%) between 2013 H1 and 2014 H2. Similar margin differences using the price gap between the before tax non-discounted gasoline pump price and the imported crude oil price are also observed.

- There is no findings to indicate changes in the volatility of Brent crude price are associated with the increase of the price gap and there is also no findings that the frequency of price adjustment behavior of the 5 oil companies is related to frequency with which the Brent crude oil price varies.

Quick going up, slow coming down

- The Council found that a significant relationship between the change in average pump price and the lagged change in the Brent crude price over the whole two year period. The Council also looked into each of the four six-month periods separately and found that for two of the periods there was a difference in the time delay between a change in crude oil price and the change in pump price depending on whether prices are increasing or decreasing - in 2013 H1 there was a delay of 4 days between a rise in the Brent oil price increases and a rise in pump price, in 2014 H2 there was a 8-day lag between a fall in crude price and the fall in pump price. These differences in delay are a possible sign of "quick going up, slow going down" however they are not stable over time.

- Different companies record different time delays in response to the Brent crude oil price changes. Some of the individual companies tend to react faster or slower regarding price change than other companies.

More going up, less coming down

- The magnitude of daily percentage change of the Brent crude oil price is usually larger than that of daily percentage change of average pump price. The International crude oil price changes every trading day but the pump price only adjusts few times a month implying that oil companies smooth out some of the day to day changes in international prices, perhaps reflecting the arrival of auto-fuel shipments to Hong Kong.

- The price gap between the pump price and the Brent crude oil price increased over last two years. 2014 H2 recorded the highest price gap between the average pump price and the Brent crude oil price. It also had the highest proportion of days with significant daily percentage decrease in the Brent crude oil price. The high price gap might be due to the decrease in the Brent crude oil price and the delayed catch up of pump prices.

- The effect of the Brent crude price on pump price could be observed from the proportion of days with significant decrease in the Brent crude price of a period is positively related to the price gap, but not the proportion of days with significant increase in the Brent crude price. The relation between the product cost margin (using import oil price) and the proportion of days with significant decrease in the Brent crude oil across periods was also found. It can be a sign of “regular going up, less coming down” or “no going up, less coming down” in the 2014 H2. It appeared in time when the Brent crude oil price changed more frequently and significantly.

Recommended Measures against the Pricing Practices

- The Government believes that in view of the import and stock-piling pattern of oil companies, there is a time lag for the adjustment of the auto-fuel import prices to be reflected in local pump prices. Therefore, the comparison has been made between the average import prices of the previous month and the local retail prices in the current month.

- The Council found the response of oil companies can be different. One improvement could disclose more frequent import oil price data perhaps for each shipment to observe whether there could be quicker response against the import price and tracking of pump price movement. Currently the import price is reported too infrequently to estimate the product cost margin as the import price data is available at least a month delay and with limited access.

- Inducing more market information available, so they could be disclosed to the public that the Council’s initiative of oil price calculator Apps and new Diesel Apps. Thus would help consumers see aspects other than price such as quality of services, variety of services and discounts in offer.

- The Government can also facilitate transparency with more information disclosure like review and publish the cost structure in the market like the “Study of the Hong Kong Auto-fuel Retail Market” released in 2006. This facilitates public understanding and scrutiny on the impact of auto-fuel price fluctuation to consumers.

Consumer Council

February 2015

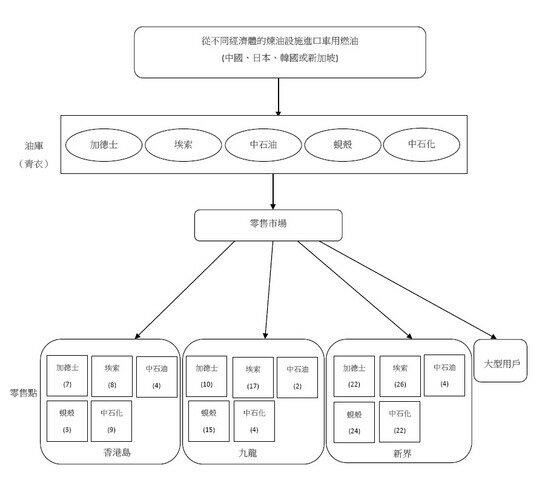

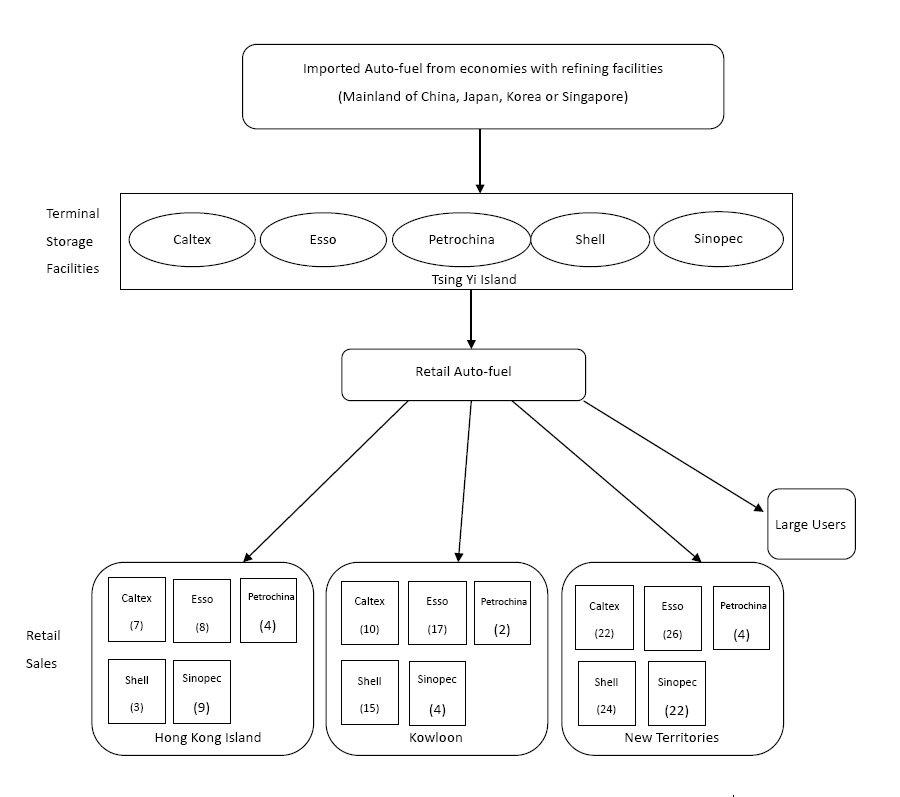

Annex 1: The Structure of the Auto-fuel Market

Note: Numbers in brackets denote the number of retail petrol filling station sites in each location.

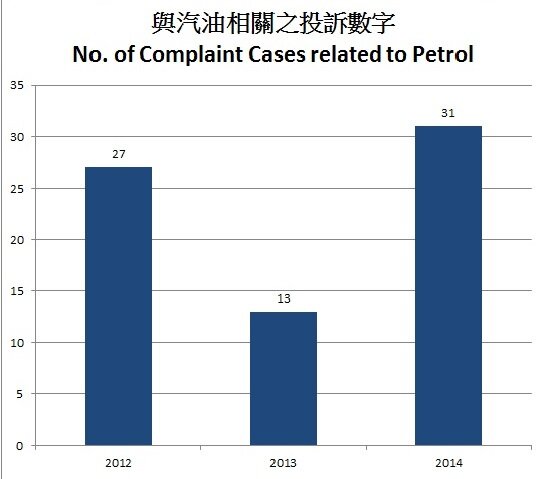

Complaint Figure

| No. of Complaint Cases related to Petrol | |||

|---|---|---|---|

| 2012 | 2013 | 2014 | |

| Case | 27 | 13 | 31 |